The first processed dairy products consumed by humans were likely cultured dairy products some 8,000 to 12,000 years ago. Nobody has quite pinned the exact date down yet. Production started at a very small scale, but the size of the market for cultured dairy products is now enormous and growing.

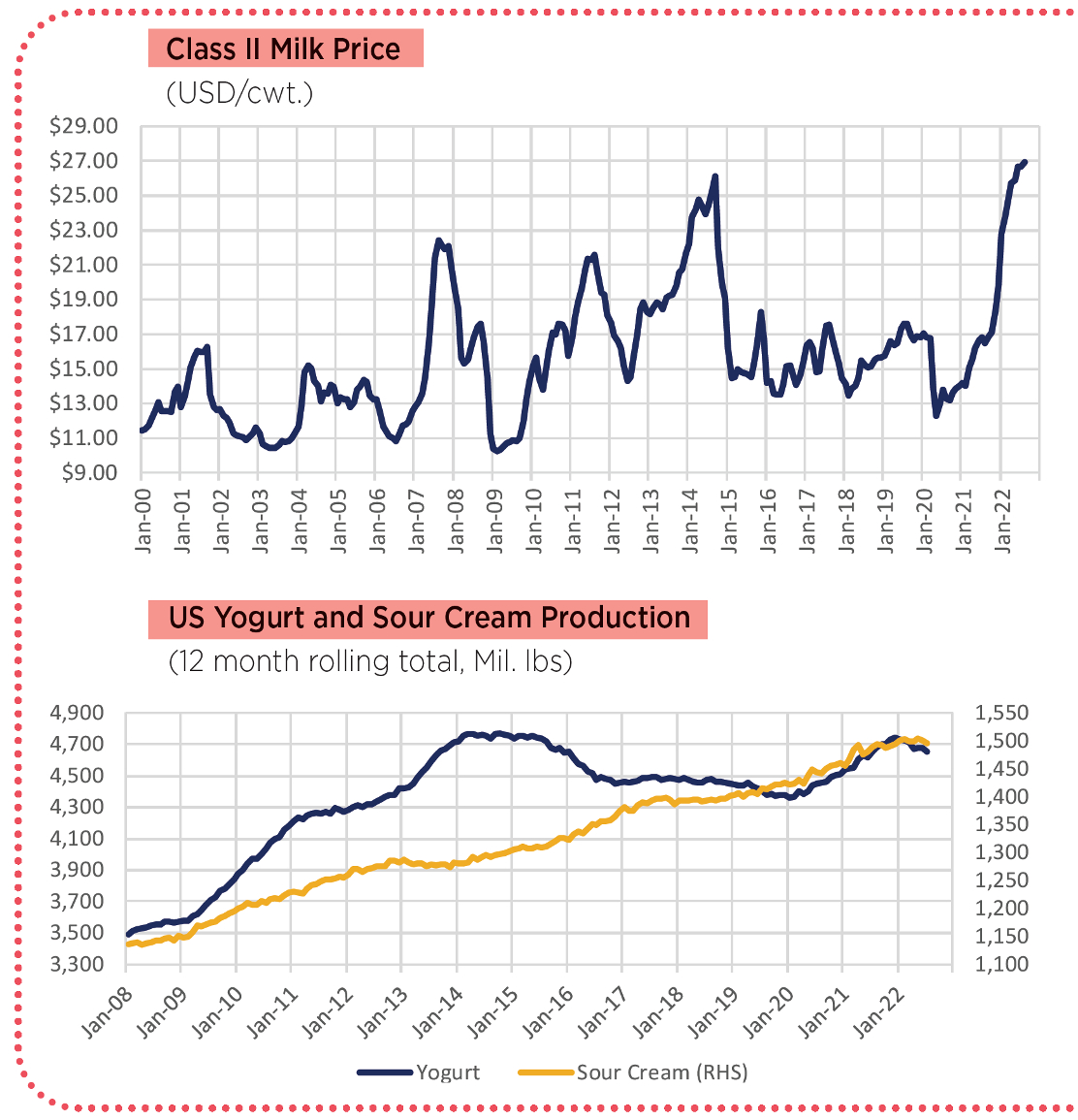

During 2021 the US produced 4.7 billion pounds of yogurt, up 5.2% from 2020, and 1.5 billion pounds of sour cream, up 2.3% from 2020. But the number that seems to be catching the most attention right now is the record high price of milk that is going into cultured dairy products.

In the US most cultured dairy product makers are operating in areas that are covered by Federal Milk Marketing Orders (FMMOs), which set a minimum price for milk each month. Milk going into these products is classified as Class II milk. The Class II milk price set new record highs in June, July and August with the year-to-date average price also at a record high, up 62.5% from last year.

We’ve had two companies recently asking about how they can hedge their Class II milk costs, and it’s clear why they are showing an interest.

Tightening stock prices

While it seems strange to the uninitiated, the price that cultured dairy product makers pay for the milk they use is tied to the price of butter and nonfat dry milk (NFDM). The price of butter is used to calculate the value of fat and the price of NFDM is used to calculate the value of protein and other solids (mostly lactose) in the milk. Most of the increase in the Class II milk price this summer was driven by rising butter prices that hit a new record high in September.

We came into the year with butter stocks already on the tight side and the market has been further tightened by weak milk production in the first half of the year and very strong butter exports. That has left the market undersupplied in the lead-up to the year-end holidays – 20% of butter is consumed in November and December.

On the bright side, lower NFDM prices, driven by weaker demand from China, should bring Class II prices down a bit in September and October despite the record high butter price. But the longer-term outlook for 2023 calls for relatively high milk prices as milk production remains weak across the major dairy exporting regions.

What can be done about the record high prices? There are futures contracts that trade on the Chicago Mercantile Exchange (CME) for Class III and Class IV milk, but they do not have a Class II contract for cultured dairy product producers. However, the CME does futures contracts for butter and NFDM that can be used to easily hedge the Class II milk price. In early September the futures market was allowing buyers to lock in a Class II milk price of about $21.80 for 2023. That is still a high price from a historical perspective, but it is a lot lower than the record high $26.91 in August this year.

- Editor’s note: This material should be construed as market commentary, merely observing economic, political and/or market conditions, and not intended to refer to any particular trading strategy, promotional element or quality of service provided by the FCM Division of StoneX Financial Inc. (“SFI”) or StoneX Markets LLC (“SXM”). SFI and SXM are not responsible for any redistribution of this material by third parties, or any trading decisions taken by persons not intended to view this material. Information contained herein was obtained from sources believed to be reliable, but is not guaranteed as to its accuracy. Contact designated personnel from SFI or SXM for specific trading advice to meet your trading preferences. These materials represent the opinions and viewpoints of the author, and do not necessarily reflect the viewpoints and trading strategies employed by SFI or SXM.

- Nate Donnay is the Director of Dairy Market Insight at StoneX Financial Inc. and has been applying his expertise in large complicated systems and statistical analysis to the international and US dairy markets since 2005. As a consultant, he has worked with clients at all levels of the dairy marketing chain from the farm level up to processors and packaged foods companies, food distributors and restaurants, as well as related industries such as banks, private equity groups, government agencies and industry associations.